Taking Your Financial Reports to the Next Level with Management Reporter – Statement of Cash Flows (6 of 8)

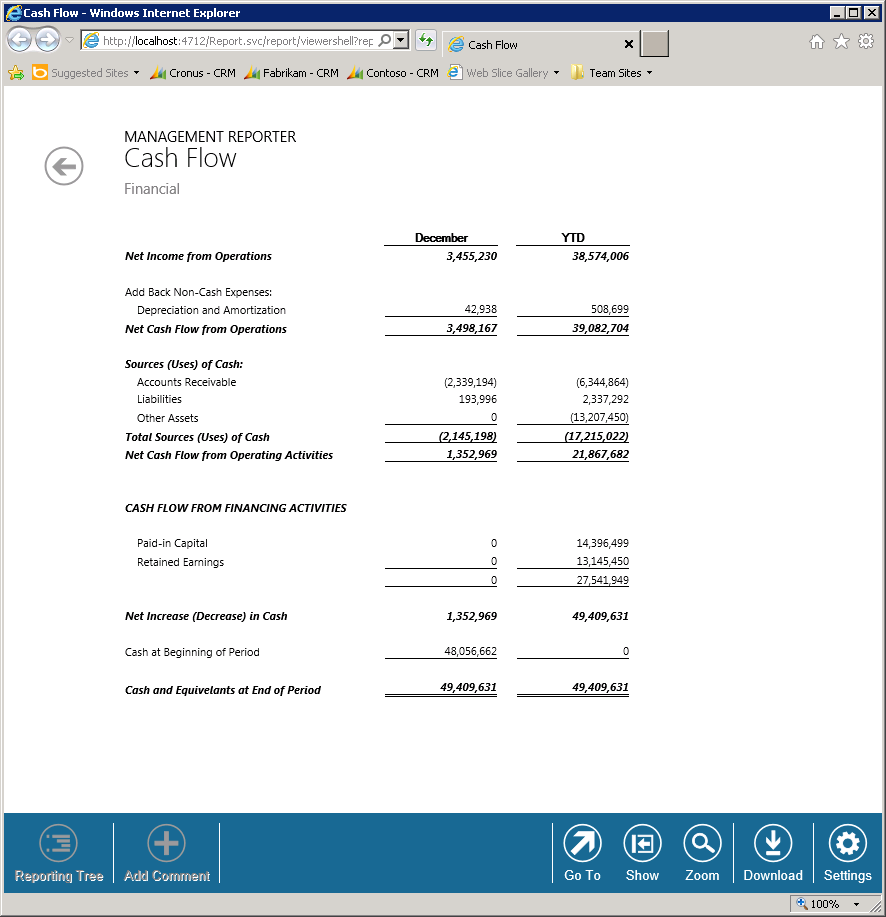

The sixth report in the “Taking your Financial Reports to the Next Level with Management Reporter” series is the “Statement of Cash Flows.” There are often multiple financial or strategic opportunities available to a company, but not a lot of cash for those opportunities. The need for sufficient cash to cover operating expenses needs to be balanced against opportunities to pay off debt or to make operating investments. The Statement of Cash Flows report helps in evaluating past operations and in planning future investing and financing activities.

This video contains how to create a Statement of Cash Flows report for your business.

[embed]https://www.youtube.com/watch?v=Ao3vszC6k7U&feature=youtu.be[/embed]

In summary, the key features included in the “Statement of Cash Flows" report were:

- Account modifier in the Row Definition to return beginning balance or year-to-date amounts for the cash accounts rows

- Non-Printing rows and columns used for calculations

- Advanced cell placement for calculating the beginning cash balance

Links to other posts in this series:

- Quarterly Revenue by Business Unit - Are we making a profit?

- Weekly Material Usage - Are we being efficient?

- Budget to Target - Are we hitting targets?

- Postings Audit - Are we entering transaction accurately?

- Statement of Cash Flow - Are we making the right investments?

- Quarterly Tax Form - Are we getting the data needed for taxes?

- Financial Matrix - How are we performing?